Most of the attention paid to American chip reshoring tracks the leading edge — the 2nm and 3nm logic that powers AI accelerators. But the part of the chip stack that actually moves with industrial production volume sits far below that frontier: the analog and embedded processors built on foundational nodes of 28nm and above. These are the power-management, signal-chain, and microcontroller parts that go into every car, every motor drive, every piece of factory automation. In 2026, Texas Instruments begins ramping a second 300mm fab in Lehi, Utah — LFAB2 — and onshores precisely this layer at scale. The complication is that it walks into a market structurally tilting toward oversupply, and the economics of the bet are anything but settled.

The asset TI underwrote

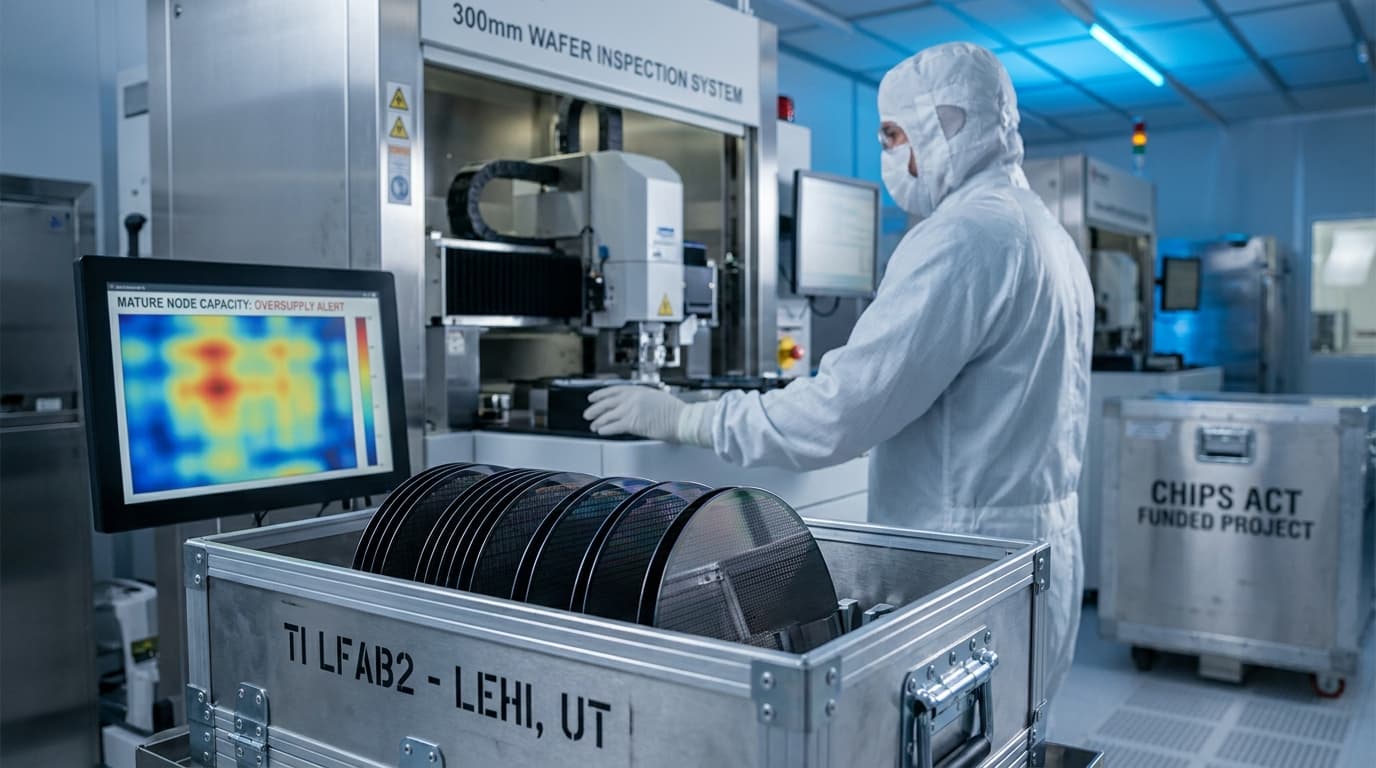

TI's roughly $11 billion investment in Lehi is the largest private capital project in Utah's history. The new fab connects to TI's existing LFAB1 in the state's Silicon Slopes corridor; construction began in the second half of 2023, with production targeted for as early as 2026. Per TI's own description of the site, Lehi is a 300mm analog and embedded-processing operation, designed to LEED Gold, adding roughly 800 direct TI jobs plus thousands of indirect jobs, and engineered to produce tens of millions of chips per day.

The wafer-size math is the whole thesis. Moving from 200mm to 300mm wafers spreads fixed cost across far more die per wafer; TI is targeting roughly 40% lower cost per chip at 300mm scale over the long term. Backing the buildout is a [$1.6 billion CHIPS Act grant](https://www.manufacturingdive.com/news/texas-instruments-chips-science-act-funding-wafers-texas-utah/724452/) supporting TI's 300mm fabs across Texas and Utah. That subsidy is already showing up in cash: TI's FY2025 free cash flow rose about 96% year over year to $2.9 billion, aided by roughly $670 million of CHIPS-related cash benefits.

The market it's walking into

The supply-side backdrop is a sustained Chinese buildout at exactly the nodes Lehi targets. China added roughly 15% foundry capacity in 2024 and about 14% in 2025, concentrated in 28/22nm and analog. By the TrendForce read, Chinese foundries are projected to exceed 25% of top-10 mature-process capacity by the end of 2025 and to reach roughly 31% of global 28nm capacity by 2027. The names driving it — SMIC, Hua Hong, Nexchip, Silan — are stepping up 12-inch mature-process capacity even as the segment consolidates.

The pricing signal that matters most: SMIC has reportedly cut 28nm wafer pricing from around $2,500 to roughly $1,500. With mature-node utilization across the industry running below about 80%, that kind of cut sustains downward pressure at the foundational layer. Trade reporting from late 2025 framed it as capacity expansion meeting weakening 28nm demand — the classic setup for a glut.

The twist that complicates the thesis

Here is where the simple "collapsing analog pricing" story breaks down. In early 2026, the direction of analog prices was up, not down. Multiple Chinese analog makers — Novosense, SG Micro, Fortior, Halo, Silan, Kiwi — raised prices, and so did TI. TI's April 2026 list adjustment raises selected products by 'as much as 85%,' attributed to rising wafer and packaging input costs and AI-related demand.

This is a near-term cost-push cycle layered on top of a long-run structural one, and the two point in opposite directions. The cost-push wave is a short-term tailwind for incumbents like TI. But the same reporting notes the increases actually help Chinese mature-node firms compete with US and EU rivals without sacrificing too much margin — meaning the price rises do not erase China's structural share gains. The cost-push cycle masks the structural pressure; it does not cancel it.

TI's economics under strain

The strain is already visible in TI's financials. Per the company's Q3 FY2025 results, gross margin fell about 2.2 points year over year to 57.4%, with operating margin down 2.3 points to 35.1%. Management explicitly attributes the compression to ramping 300mm capacity and underutilization — citing Lehi underutilization as a drag on embedded margins. In other words, TI is paying the cost of empty capacity today against the promise of that 40%-lower cost-per-chip tomorrow.

The demand side gives it room to be patient. TI's Q2 2025 analog revenue was $3.452 billion, up 18% year over year, and the company ended Q2 with $4.8 billion of inventory — about 222 days — positioned intentionally across nodes. That is a deliberate bet: carry inventory and absorb underutilization now, on the view that scale economics and an eventual utilization recovery clear the math. What has to happen for the bet to pay off is straightforward to state and hard to guarantee — Lehi has to fill up.

Is the glut even real?

It's worth presenting the overcapacity question as contested rather than settled. Analysts at CSIS, in a closer look at legacy-chip overcapacity, argue that fears of a Chinese mature-node glut may be overstated once you account for genuine demand absorption. The price-war evidence — SMIC's wafer cuts, sub-80% utilization — points one way; the skeptical view points another. The honest framing is that both signals are live at once, and the 2026 price-rise cycle is itself a data point cutting against the simplest glut narrative.

Operator takeaways

For buyers of analog and embedded parts, the calculus is a trade-off between supply security and pricing risk. Subsidized domestic 300mm capacity at Lehi is a hedge against supply-chain disruption and a source of geographically diversified parts. But the open question for procurement and investors alike is whether that capacity rides its structural cost advantage cleanly through the cycle — or whether it runs below breakeven to defend share against Chinese competitors who keep adding mature-node capacity regardless of where prices sit this quarter.

The core tension does not resolve neatly: does CHIPS-subsidized domestic analog capacity survive a Chinese oversupply cycle on structural cost advantage, or does the current price-rise cycle merely mask a coming margin squeeze at the lowest-margin layer of the stack?

Signposts to watch in 2026–2027

-

TI utilization recovery. Watch whether the Lehi-driven margin drag in TI's quarterly results narrows as the fab fills — the single clearest read on whether the scale bet is paying off.

-

China 28nm share milestones. Track progress toward the projected 25%+ of top-10 mature capacity by end-2025 and ~31% of global 28nm by 2027.

-

Whether the price-rise cycle reverses. The April 2026 analog increases are cost-push driven; if input costs ease and AI-related demand cools while Chinese capacity keeps landing, the structural pressure reasserts itself.

Related reading

-

[Samsung's $44B Taylor Fab Slips 2nm Mass Production to 2027 — An Order-Book Problem, Not a Construction One](/article/samsung-taylor-fab-2nm-mass-production-2027-order-book)

-

[The $1.77 Trillion Reshoring Boom Isn't Showing Up in the Concrete](/article/reshoring-boom-factory-construction-spending-falling)

-

[Micron Breaks Ground on Clay, NY Megafab — and the Onondaga Workforce Pipeline Is Counting Graduates in Dozens](/article/micron-clay-megafab-groundbreaking-onondaga-workforce-gap)

Sources

-

Texas Instruments to build $11B semiconductor plant in Utah — Construction Dive

-

Texas Instruments scores $1.6B in CHIPS funding — Manufacturing Dive

-

China capacity expansion and weakening demand prompt cost reductions for 28nm — DigiTimes

-

China's mature-node push: Nexchip, Silan, Hua Hong step up capacity — DigiTimes

-

China's Low-Cost SiC and Mature Chips Ignite Global Semiconductor Price War — TrendForce

-

Chinese analogue chipmakers join wave of global price rises — South China Morning Post