The narrative around the AI buildout has fixated on GPUs, fab capacity, and grid interconnect queues. The harder constraint is now sitting in two American industrial campuses — Caterpillar's Large Engine Center in Lafayette, Indiana, and Cummins' high-horsepower plant in Seymour — where order books for the diesel and gas reciprocating engines that backstop hyperscale data centers have run past the point that incremental customers can be served on any reasonable timeline.

Caterpillar's Q1 2026 10-Q reported a record $63 billion backlog, up roughly 79% year-over-year, with the Energy & Transportation segment singled out for data-center-driven power generation demand. Cummins' large genset allocation has reportedly slipped into 2028. Across the major Western OEMs, lead times for large units now sit in a 40 to 107-week band. For a hyperscaler trying to commission a campus in 2027, that means the engines have to be ordered before the dirt moves.

Sizing the queue

The order book is not abstract. Caterpillar's record backlog has shifted the company's revenue mix toward stationary power, and analyst coverage has begun framing the equity as a de facto AI infrastructure name rather than a pure construction-and-mining cyclical. Energy & Transportation is the segment doing the work.

Cummins has been more direct about the cause. The company's own commentary on AI-driven infrastructure design pitches the OEM as a strategic partner to the hyperscalers, but the supply-side reality is allocation. New U.S. customers seeking large gensets are being quoted delivery windows that compete with the multi-year utility interconnect timelines they were trying to route around.

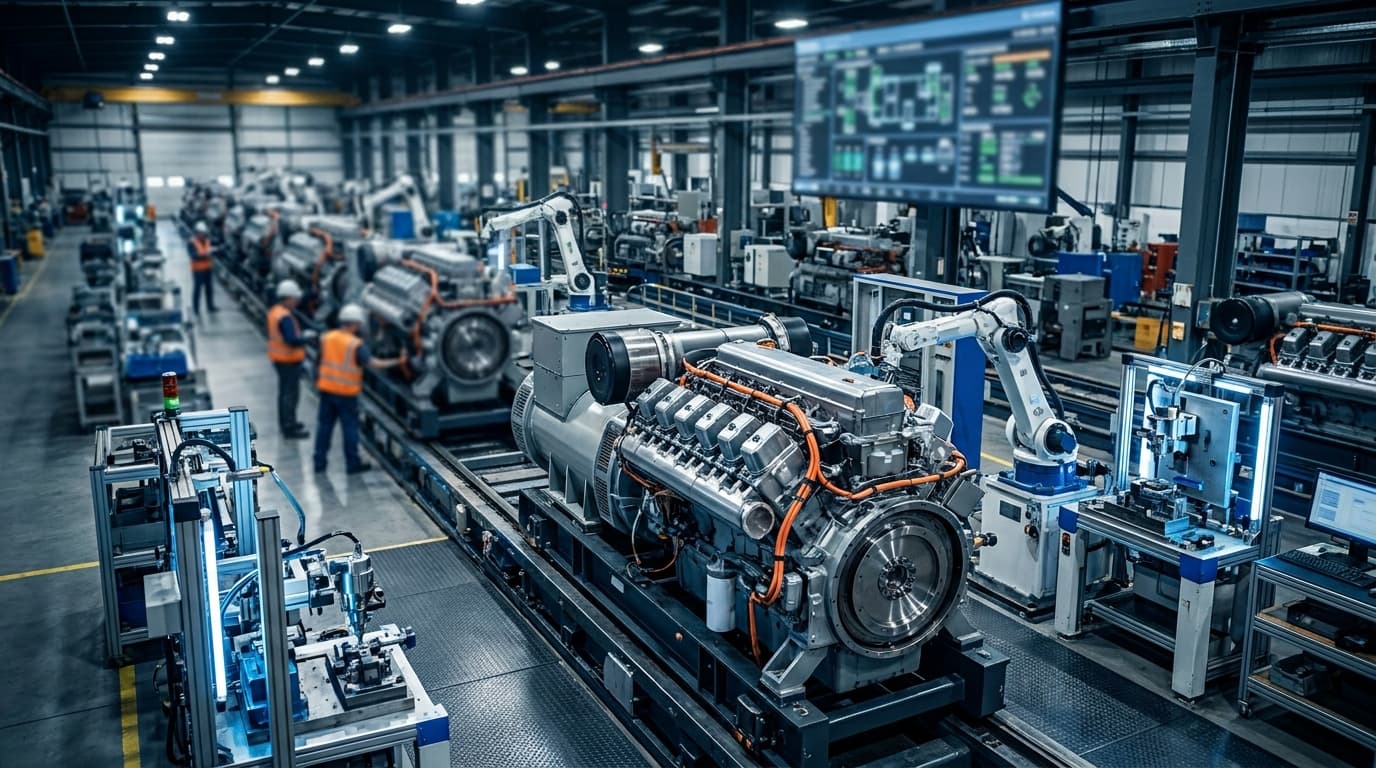

Lafayette: anatomy of a $725 million expansion

Caterpillar's response is concrete. The company broke ground on a $725 million expansion of its Lafayette, Indiana Large Engine Center — a new 300,000 square foot building, roughly 100 new positions on top of an existing 1,900, with the building targeted for completion by the end of 2026 and new equipment installed through 2027. Trade press has corroborated the timeline and the explicit data-center rationale.

Caterpillar is targeting roughly a tripling of large reciprocating engine output, with an incremental ~15 GW of annual capacity earmarked for the AI/data center segment. That figure is what it takes to clear the queue — and it does not arrive until 2027 at the earliest.

Seymour: Cummins' high-horsepower campus

Cummins' Seymour, Indiana plant produces 19L through 95L high-horsepower engines for power generation. The company has put more than $350 million into the campus over the past decade, including a recent $25 million-plus expansion to launch a new platform in 2024. Trade-press accounts describe the upgrade as a direct response to power-gen demand.

What Seymour does not appear to have, at least publicly, is the kind of step-change capital infusion that Lafayette is getting. That has implications for how the backlog clears: even with the new platform online, Cummins is rationing.

Where the bottleneck has migrated

The choke point has begun to move downstream of the OEMs themselves. Operators in the supply chain point to large iron castings, alternator copper, switchgear, and tier-2 machining capacity as the next binding constraints. Investigative reporting on permits filed for the Stargate buildout has flagged Generac engines turning up in places the market would not normally expect — a tell that procurement is reaching past first-choice suppliers to fill specs.

Direct OEM equity into tier-2 forging or machining suppliers has been discussed in the industry but is not, as of this writing, publicly confirmed at scale. That is the part of the supply-chain story worth watching: whether Caterpillar and Cummins move from buying capacity to financing it.

Overflow capacity: Rolls-Royce mtu and the gas pivot

Rolls-Royce Power Systems has positioned its mtu brand as the relief valve. The company committed $24 million to expand Series 4000 production in Mankato, Minnesota, including a 250,000 square foot Logistics Operations Center, targeting more than a 120% production increase by 2026. Independent trade coverage describes the move explicitly as positioning to absorb Cat and Cummins overflow.

The product side is moving too. The new 20-cylinder mtu Series 4000 L64, launching for the 60 Hz North American market in 2026, delivers 2.8 MW in 45 seconds; the gas variant offers a 120-second fast-start spec. Kohler-SDMO sells data center power systems globally but has not announced a U.S. capacity expansion at the scale of the three OEMs above.

Diesel-to-gas, and the move from backup to prime

The deeper structural shift is that gensets are no longer just backup. Hyperscalers facing three to seven-year utility interconnect quotes are pivoting to natural-gas turbines and reciprocating engines for prime power — running on-site generation as the primary source while the grid catches up, or indefinitely. That changes the duty cycle, the emissions profile, and the parts of the supply chain that get squeezed.

Virginia, the largest global data center market, had more than 10,500 generator units permitted with roughly 27 GW of backup capacity by the end of 2025. That installed base is now being reframed as latent prime-power capacity, with the gas-genset product roadmap from mtu and others built around it.

Implications and risk

For U.S. heavy-industrial suppliers, the read is straightforward: mid-cap forgers, foundries, alternator manufacturers, and switchgear OEMs are the next-leg beneficiaries of capex that has already been committed at the engine OEM level. Generac's appearance in Stargate permits is one data point that procurement is broadening.

The risk sits on the timeline. The new Lafayette capacity arrives in 2026–2027. Rolls-Royce hits its Mankato target in 2026. Cummins' Seymour platform is already running. If AI capex flattens before that capacity comes online, the OEMs absorb under-utilization on plants sized for a demand curve that did not hold. If it does not flatten, the backlog clears slowly, and the marginal hyperscale buildout in 2027 still has to find an engine.

Related reading

-

Foxconn's Wisconsin Pivot to AI Server Assembly Quietly Hits Full Tilt

-

U.S. Battery Cell Capacity Is Now Outrunning Demand — and the First Gigafactory Lines Are Going Cold

-

Intel's Ohio Slip to 2030 Forces Commerce to Convert Its Biggest CHIPS Bet into Equity